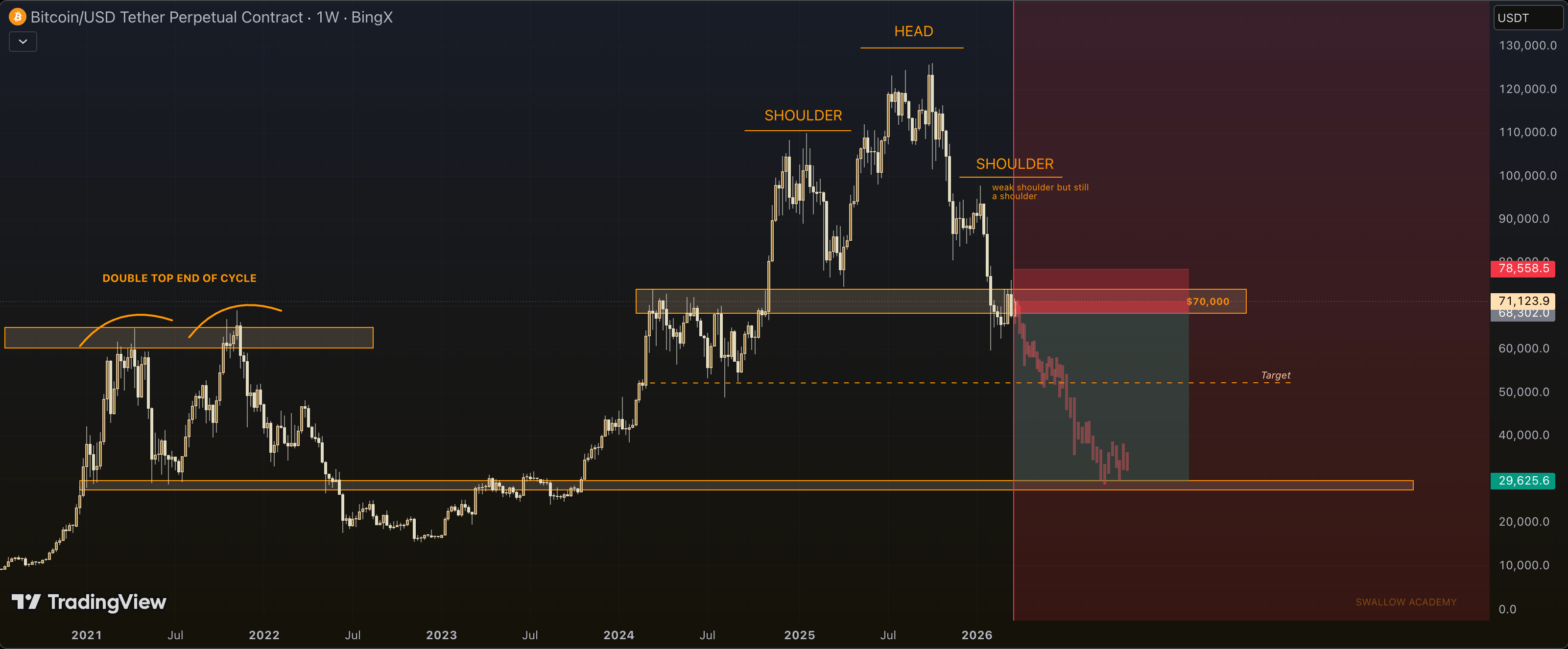

Lo, the charts on TradingView reveal a pattern so comical, so tragically human, that one might mistake it for a caricature in a St. Petersburg tavern. A Head and Shoulders, they call it-a formation as grandiose as a nobleman’s wig, yet as fragile as a bureaucrat’s ego. The first shoulder, formed in the halcyon days of 2025, was but a prelude. The head, a towering monument to greed, emerged when Bitcoin reached its zenith. And then, in 2026, the second shoulder, a weak and pitiful thing, completed this farcical tableau. The analyst, with a shrug as eloquent as a Gogol protagonist’s sigh, admits its frailty but insists it is a shoulder nonetheless. And so, the pattern is complete, a prophecy of woe: Bitcoin, once a titan, now teeters on the brink of collapse.