Ah, the modern investor’s dilemma: to ride the tempestuous seas of Bitcoin with MicroStrategy’s MSTR, or to lounge in the steady cabin of STRC, sipping dividends while the ship careens onward. Strategy Inc., that audacious navigator of financial fancies, offers two berths on its Bitcoin galleon-one for the daredevil, the other for the dilettante.

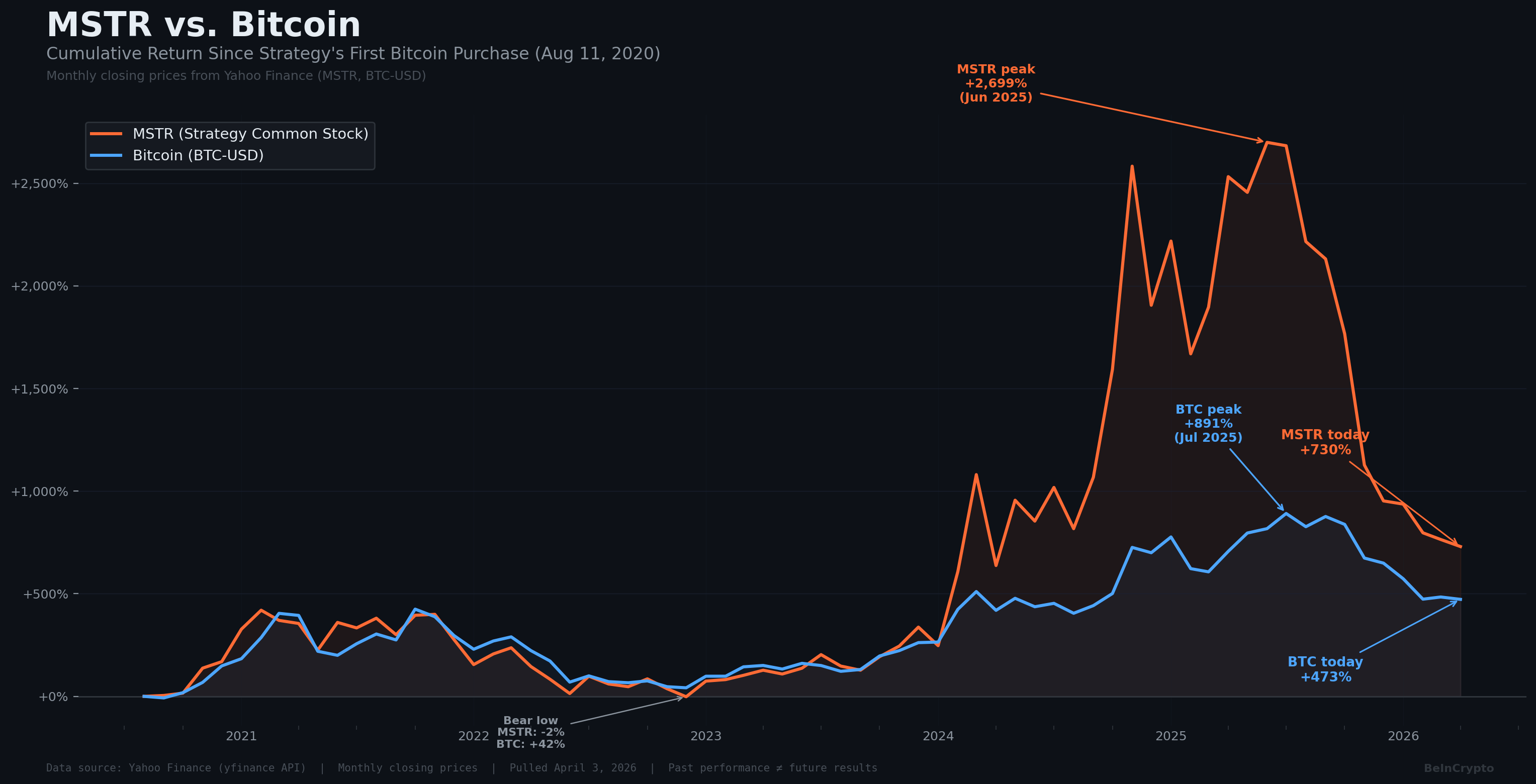

Behold, the erstwhile MicroStrategy, now a veritable treasure chest of 762,099 BTC, acquired at the princely sum of $75,694 per coin. A hoard valued at $51 billion, no less, backing both its common stock (MSTR) and its perpetual preferred shares, the aptly named Stretch (STRC). The same vessel, yet two voyages so disparate they might as well be bound for different hemispheres. The choice, dear reader, is yours-and it may well be the most consequential decision you make this annum, provided you are of the Bitcoin-besotted persuasion.

Two Tickets, One Treasure, Divergent Destinies

MSTR, the wild stallion of the portfolio, is for those who thrill at the prospect of financial vertigo. Strategy issues shares and debt with abandon, plowing the proceeds into more Bitcoin, thereby amplifying every market hiccup into a seismic event. In bull markets, MSTR has galloped ahead of BTC by 1.5x to 3x. In downturns, it plummets with equal fervor. Debt, that ever-present specter, looms over common equity, and the relentless dilution from capital raises ensures that losses are compounded when Bitcoin stalls or, heaven forbid, retreats.

No dividend, no yield, no safety net. MSTR is the financial equivalent of tightrope walking without a net. When Bitcoin soars, the rewards are as extravagant as a Waugh novel. When it falters, well, the past six months have been a masterclass in schadenfreude.

STRC, by contrast, is the financial equivalent of a warm bath on a chilly evening. Launched in July 2025 with a 9% dividend, this perpetual preferred stock doles out monthly cash distributions, adjusting its yield to keep shares trading near the par value of $100. The dividend rate has climbed through seven consecutive monthly increases to 11.5%, where it has held steady-a testament to the mechanism’s efficacy. Predictable, boring, and oh-so-profitable. Just the thing for those who prefer their investments as steady as a Waugh protagonist’s disdain for modernity.

Stretch Dividend Rate maintained at 11.50% for April 2026. $STRC

– Michael Saylor (@saylor) April 1, 2026

The rules are as clear as a Waugh plot: if STRC’s 30-day volume-weighted average price dips below $95, the board recommends a dividend hike of 50 basis points or more. Between $99 and $101, all is well. Above $101, a cut becomes possible. Bitcoin’s daily price swings are stripped out, replaced by the soothing regularity of monthly income. It’s the financial equivalent of a sedative-effective, if not exactly exhilarating.

Strategy CEO Phong Le noted in March that roughly 80% of STRC holders are retail investors, compared to 40% for MSTR common shares. Retail, it seems, prefers the comfort of low volatility and high yield to the rollercoaster of MSTR.

~ 40% of $MSTR shares are owned by retail. ~ 80% of $STRC shares are owned by retail. Retail investors prefer low-volatility, high-yield digital credit.

– Phong Le (@phongle) March 26, 2026

Follow us on X to get the latest news as it happens

The market, that great arbiter of human folly, is sorting itself. Investors are self-selecting into the instruments that align with their financial temperament-or, more accurately, their tolerance for sleepless nights. As Bitcoin advocate Halston Valencia so aptly put it, “$MSTR is for people so convinced of bitcoin they want leveraged exposure to it… $STRC is for people who believe in bitcoin but want yield, not volatility.”

The Numbers: A Tale of Two Journeys

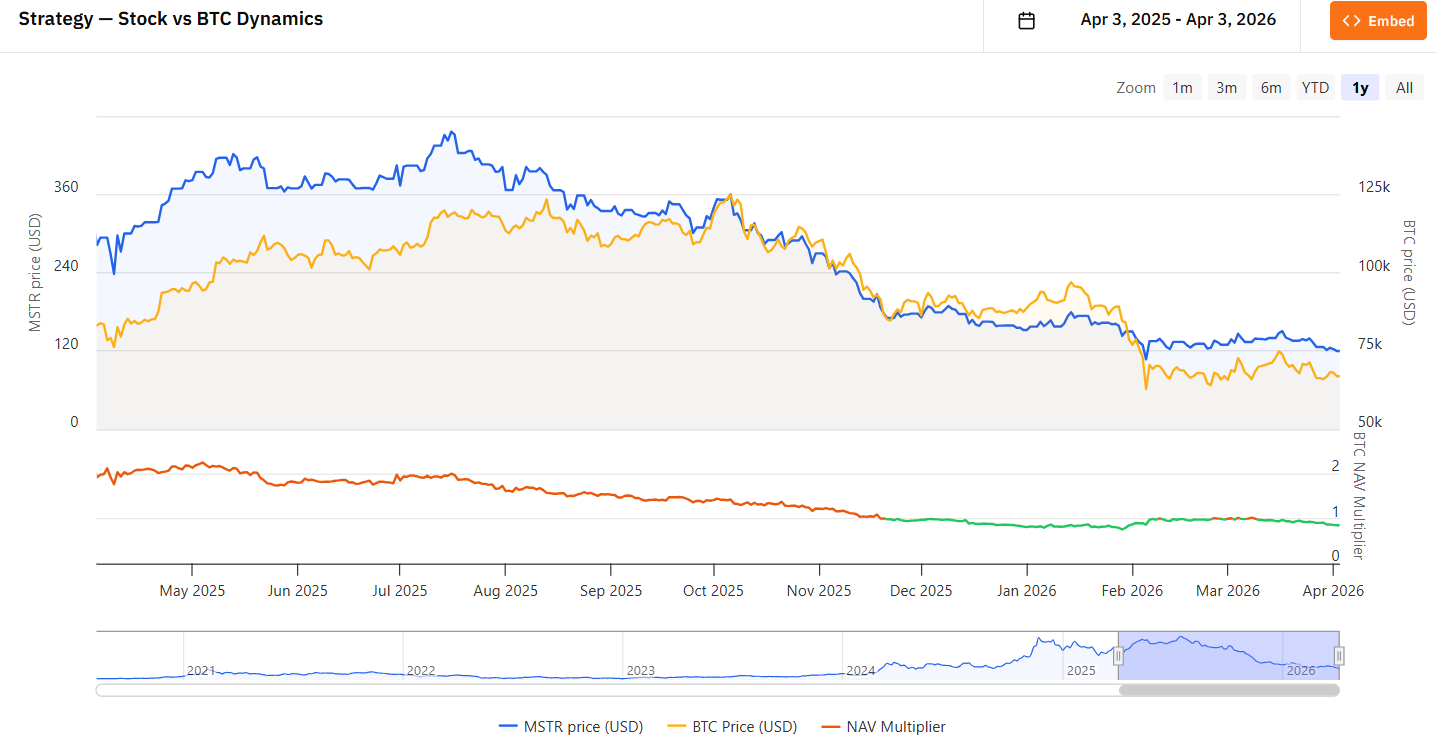

MSTR closed April 2 at $119.13, within a tight range of $116.40 to $120.22. The stock has plummeted roughly 56% over the past six months and is 74% below its 52-week high of $457.22. Leverage, that double-edged sword, has worked its dark magic in reverse. STRC, meanwhile, traded flat at $100.00 on the same day. Its entire 52-week range spans just $88.00 to $100.42. Year-to-date returns sit near 4%, almost all from dividends rather than price movement. Boring by design, profitable by intent.

Benchmark-StoneX equity research analyst Mark Palmer described MSTR as a leveraged, non-yielding Bitcoin proxy better suited for sophisticated, risk-tolerant investors. STRC, he noted, maps to how most retail investors actually think about income-predictable, secure, and heavily overcollateralized.

🧵 7/7 🌍 The TL;DR: STRC is the ultimate bridge between TradFi yield and a Bitcoin-native balance sheet.

As Benchmark analyst Mark Palmer notes, STRC is a key driver for expanding Strategy’s Bitcoin holdings while minimizing the dilution of common shares. It offers the…

– PreferredPath (@PreferredPath) March 11, 2026

Overcollateralization, that financial bulwark, is key. Strategy maintains $2.25 billion in cash reserves to service dividend payments, and its BTC treasury dwarfs STRC’s $5 billion notional market cap many times over. Even in a severe Bitcoin drawdown, the preferred stock sits senior to common equity in the capital structure. MSTR holders, poor souls, absorb losses first.

The capital structure adds another layer to that thesis. Preferred holders sit senior to equity. Even a severe BTC correction that wipes out MSTR common equity creates a much higher failure threshold before it reaches the preferred dividend. He built the risk in layers.

– Collin 🍊 (@STRchitect) March 31, 2026

Strategy also announced a $42 billion at-the-market program, split evenly between common stock and STRC issuance, to continue its march toward 1 million BTC. STRC, it seems, is not just an income instrument but the primary funding engine for the next phase of Bitcoin accumulation.

Growth or Income: The Eternal Conundrum

The decision, in the end, comes down to temperament, not conviction. Both MSTR and STRC holders are Bitcoin believers; they simply disagree on how to express that belief in their portfolios. MSTR rewards patience and iron nerves. If Bitcoin recovers from its current range near $67,000 and pushes past previous highs, MSTR holders stand to capture outsized gains that no preferred stock or spot holding can match. Historically, MSTR has delivered returns exceeding 3,000% over multi-year bull cycles, while BTC itself returned around 900%.

However, the current balance sheet tells a different story. Strategy’s BTC holdings carry unrealized losses exceeding $5.5 billion. The company paused its 13-week Bitcoin buying streak last week, and insider selling has surfaced, with board director Jarrod Patten offloading 2,100 shares. The stock trades below all major moving averages, with weak momentum indicators.

STRC, on the other hand, rewards consistency and discipline. The 11.5% annualized yield, paid monthly at roughly $0.96 per share, functions more like a high-yield credit instrument than an equity position. After each ex-dividend date, when the price typically dips, STRC has recovered to par within nine to twelve trading days. Dividends have so far been classified as non-taxable return of capital, reducing holders’ cost basis rather than generating immediate tax liability.

The trade-off is clear:

- STRC holders will never capture a Bitcoin moonshot.

- The price is engineered to stay near $100.

- The upside is capped.

- The income is the entire point.

The Bigger Picture: A Symphony of Interests

In March alone, STRC issuance funded $1.18 billion in Bitcoin purchases, roughly 16,800 BTC. Common stock sales raised just $396 million during the same period. STRC holders are now the primary source of capital fueling Strategy’s accumulation machine.

Here it is.

More than 0.1% of the entire Bitcoin supply in a single week.

Strategy’s largest Bitcoin purchase since 2024.

A massive $1.18bn from $STRC with the common stock $MSTR raising $396m.

We are living in historic times.

Absolutely incredible.

– Zynx (@ZynxBTC) March 16, 2026

This shift changes the relationship between the two instruments. MSTR benefits when STRC attracts more capital, as more STRC issuance means more Bitcoin purchased without diluting common shareholders as heavily. STRC benefits when Bitcoin appreciates, as the treasury backing its dividends grows stronger. They feed each other, a financial pas de deux.

A growing number of investors hold both, alongside spot Bitcoin in self-custody:

- Leveraged upside through MSTR

- Steady income through STRC, and

- Pure sovereignty through direct BTC ownership.

The three do not compete for the same dollar. They serve different parts of the same conviction. The infighting between Bitcoin maximalists who reject financial products and those who adopt them misses the structural reality. All three paths drive more Bitcoin demand. All three benefit from the same treasury growth.

The only real question is which mix matches the investor holding the portfolio. No single answer fits everyone. But ignoring one side of the equation means leaving either growth or income on the table. And in the world of finance, as in the world of Waugh, such oversight is the mark of a fool.

Read More

- ‘Project Hail Mary’s Unexpected Post-Credits Scene Is Worth Sticking Around

- Beyond Accuracy: Gauging Trust in Human-AI Teams

- Gold Rate Forecast

- The most surprising Hannah Montana cameos: From John Cena to Dwayne Johnson and even a Coronation Street soap star as show celebrates its 20th anniversary

- Limbus Company 2026 Roadmap Revealed

- EMEA Masters Winter 2026 introduces official Qualifier for Esports World Cup

- Genshin Impact Version 6.5 Leaks: List of Upcoming banners, Maps, Endgame updates and more

- Brawl Stars Sands of Time Brawl Pass brings Sandstalker Lily and Sultan Cordelius sets, along with chromas and more

- Total Football free codes and how to redeem them (March 2026)

- Brawl Stars Brawl Cup Pro Pass arrives with the Dragon Crow skin and Chroma, unique cosmetics, and more rewards

2026-04-03 12:59