Finance

What ho, old sport:

- While the Twitterati frolicked in their conspiracy grotto, Polymarket’s betting slips remained as dry as a vicar’s sense of humor, pricing Netanyahu’s departure at a mere 4-5%. Quite the damp squib for the rumormongers.

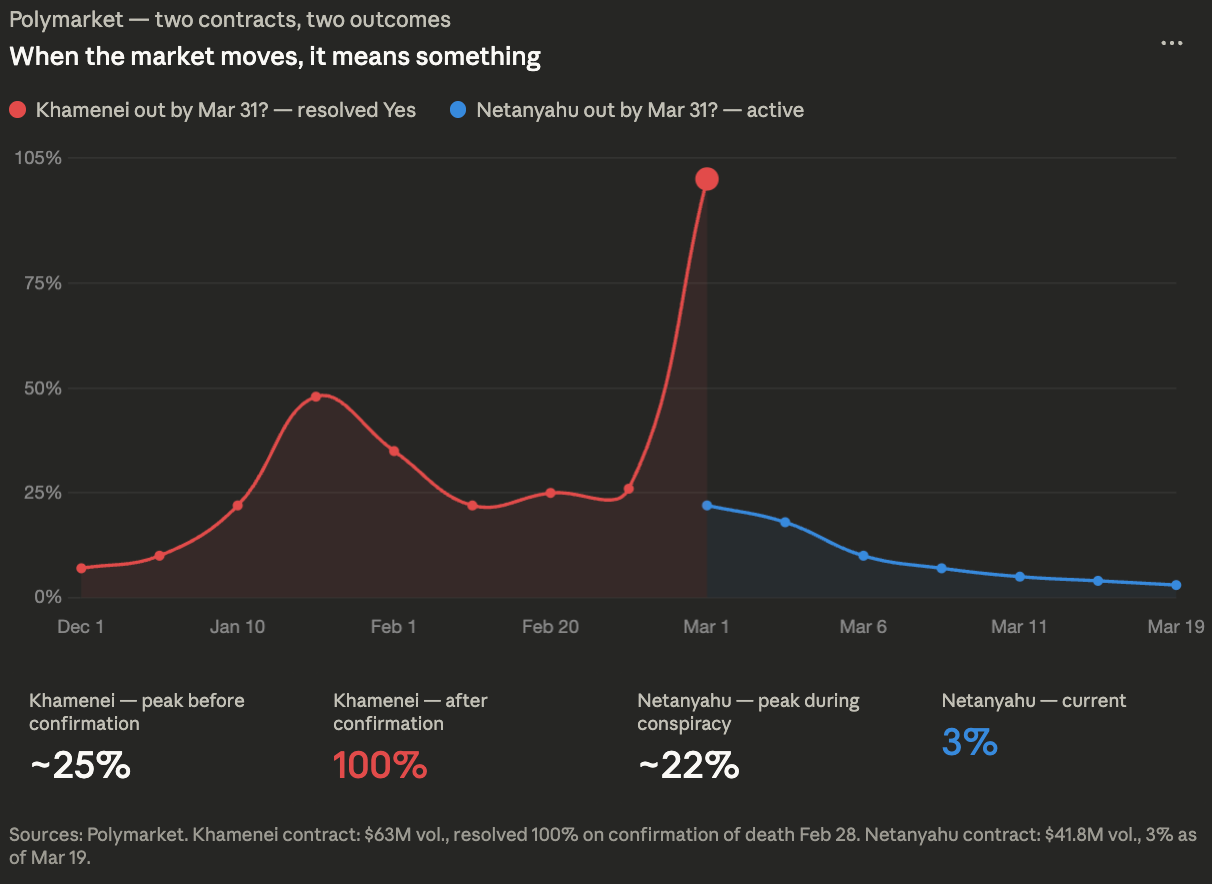

- Contrast this with the Khamenei kerfuffle: when the Iranian chap actually shuffled off, Polymarket spiked faster than a Bright Young Thing at a cocktail party. The same crowd that ignored Netanyahu’s “death” suddenly found their pricing mettle.

- Now, the political busybodies are in a tizzy, demanding these markets be shut down. Just as they’re proving rather useful, what?

The whole affair began with the sort of wartime nonsense one expects from people who read too many thrillers. Iran’s Revolutionary Guard (those charming fellows) claimed they’d struck Netanyahu’s office. Then came the forged screenshots-fake posts announcing his demise. The pièce de résistance? An AI-fueled furore over a blurry press conference frame, where Netanyahu’s hand allegedly sported six fingers. The contrarians, naturally, declared victory.

Candace Owens, that tireless siren of the conservative set, took to X (formerly Twitter, darling) demanding to know Netanyahu’s whereabouts. Iran’s Tasnim News Agency, run by the Guard, published a screed titled “New Video of Netanyahu Proves Fake,” dissecting a coffee shop clip with the zeal of a schoolmaster marking a particularly poor essay. Every refutation, of course, was met with fresh conspiracy fodder. It was all rather exhausting.

But while the fact-checkers scrambled and the podcasters prattled on, Polymarket offered a clear signal. The “Netanyahu out by March 31” contract traded at 4-5 cents, implying a 4-5% chance of his departure. The market didn’t budge. For anyone with half a brain, the conspiracy collapsed like a poorly constructed soufflé.

A record-breaking backdrop, old boy

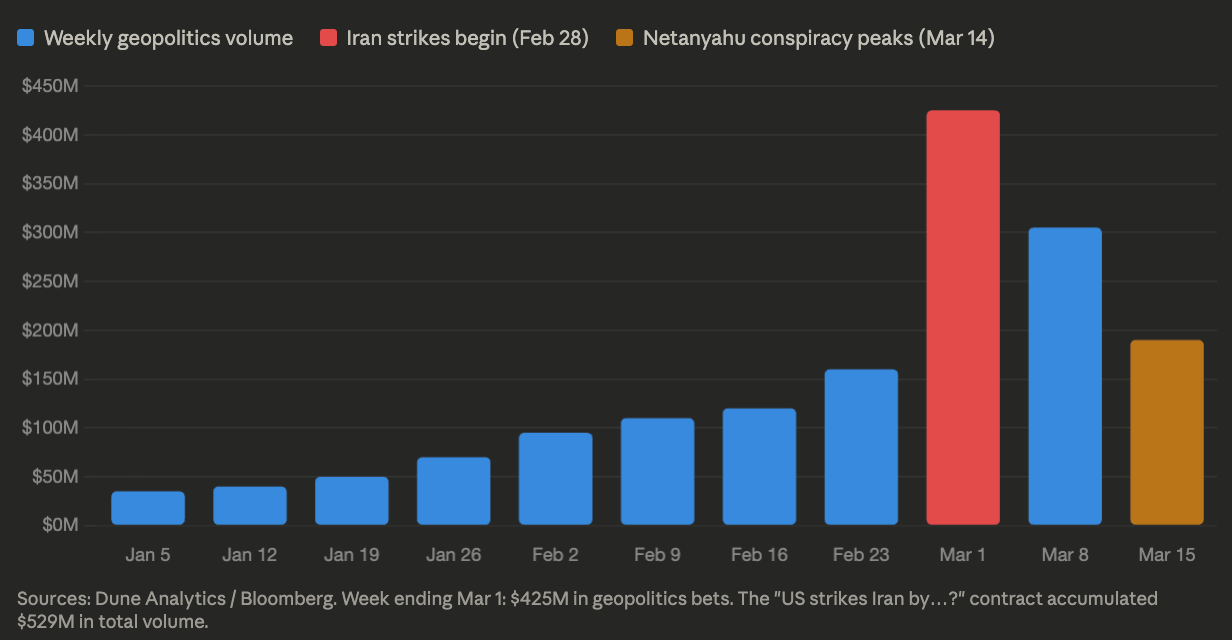

To understand why this nonsense took hold, one must consider the information environment-a veritable swamp of speculation. Since the U.S. and Israel began their Iranian adventures on Feb. 28, Polymarket has become something of a geopolitical oracle. In the week ending March 1, bettors wagered $425 million on geopolitics alone, up from $163 million the previous week. Total platform wagering hit a record $2.4 billion. The “US strikes Iran by…?” contract accumulated $529 million, making it one of Polymarket’s largest markets.

Quite the trajectory for a platform that processed $73 million in 2023 and was pushed offshore by a CFTC settlement. By 2025, it had processed $22 billion in notional trading volume. The Intercontinental Exchange, parent of the NYSE, invested $2 billion at a $9 billion valuation. When the Iran war began, equity and oil futures markets were closed. Polymarket was not.

The market as instant truth machine, what?

Prediction markets don’t deal in death contracts, per se. Polymarket offers “politician out by X date” markets, resolving “Yes” if a leader resigns, is removed, or steps down. But in a context where the conspiracy is that Netanyahu has been killed and the government is covering it up, these contracts are a splendid proxy.

The logic is simple: a dead leader cannot run a country indefinitely. Eventually, a resignation or leak would surface. A “Yes” share at 5 cents would pay out $1-a 20-to-1 return. One trader placed $151,000 on Netanyahu being out by March 31, accumulating 3.8 million shares at 4.7 cents each. If correct, the payout would be $3.8 million. Currently, it’s underwater by $26,000. The ceiling of rational conviction in the conspiracy, old sport.

At the height of the hysteria, the most aggressive speculator staked $150,000-implying long odds. The market put the probability at 5%. Social media declared it certain. The money said otherwise.

“Whether a politician is in or out of office is economically meaningful,” said Aaron Brogan, a managing attorney. “These markets accommodate that.”

Why the odds are hard to fake, eh?

The 2024 US election offered a masterclass in market efficiency. When Polymarket showed Trump trading at a premium over Harris, critics cried manipulation. A French trader, they alleged, had pumped Trump’s odds. Experts weren’t convinced. A true manipulator would pile in blindly; the French trader split orders strategically. Profit-seeking, not propaganda.

Manipulation struggles due to expected value arbitrage. If a price is inflated, traders exploit the gap until it closes. Cross-market arbitrage reinforces this: Polymarket prices against Kalshi, Betfair, and others. If odds drift out of line, traders synchronize markets toward consensus.

Harry Crane, a statistics professor, sees the Netanyahu episode as illustrative. “These markets counter propaganda because their resolution rules anchor outcomes to verifiable sources,” he said. “Governments want to limit them because verifiable price signals are harder to control.”

The Netanyahu conspiracy required a cover-up so total that no verifiable evidence would surface. An unfalsifiable claim-one no rational actor should stake capital on. This is where the conspiracy fell apart. The market priced it at 5 cents. It was right.

The contrast case: Khamenei

When Khamenei was killed, the “Khamenei out by March 31” contract spiked to 100%. It drew $45 million in volume. The top trader made $757,000. Four others cleared six figures. The Netanyahu market remained below 5 cents. The crowd that priced Khamenei’s death correctly declined to move on Netanyahu.

The regulatory storm, old bean

The informational value of these markets is being tested as political pressure mounts. When Khamenei was killed, Kalshi invoked a “death carveout,” settling positions at 39.5 cents rather than $1. Polymarket paid out in full. A $54 million lawsuit followed.

Kalshi disputes the characterization. “Our rules were clear,” a spokesperson said. They reimbursed fees and losses, ensuring no user lost money. Six Democratic senators, led by Adam Schiff, demand a ban on contracts tied to death. Merkley and Klobuchar introduced the End Prediction Market Corruption Act, citing well-timed wagers.

Brogan is skeptical of the legislative push. “This is largely Democrats generating political capital,” he said. “Without a calamity, I don’t think it passes.” Polymarket, offshore and unregulated, faces less exposure than Kalshi, which is CFTC-regulated.

Crane is clear: “These markets have genuine informational value and can counter propaganda. That’s the case study here.”

Arizona charged Kalshi with illegal gambling, part of a conflict between states and federal prediction markets. “The question is whether federal law preempts state law,” Brogan said. “Courts are hearing that now.”

What the crowd gets right-and what it can’t fix

Prediction markets aren’t infallible. Nearly 25% of Polymarket’s volume has been wash trading-artificial activity for token airdrops. A coordinated disinformation campaign could, in theory, move a market. But the Netanyahu contract had enough liquidity to make that expensive.

What markets cannot do is replace the information infrastructure they depend on. They resolve against credible sources. If those sources are corrupted or silent, the market’s signal is only as good as its resolution criteria.

In the Netanyahu case, the conspiracy required a cover-up so comprehensive that no one would find confirmation. The market priced it at 5 cents. It was right. When Candace Owens demanded to know where Bibi was, Polymarket had the answer. It just costs a few pennies to read it.

2026-03-21 19:12